STEEL: Ahhh…The Real Problem

Our version of Lions, and tigers, and bears! Oh my!...plays out like this: China, and Korea, and Turkey! Oh my! The raging debate about trade laws and our inability to enforce those laws is a most legitimate debate. One look at the following graph suggests something just doesn’t pass the smell test.

In my classroom, I speak of monopolies, oligopolies and duopolies with both definition and examples. I then answer the ubiquitous follow-up question: Yes, this will be on the final (-: Monopolies, when present in the private sector, risk price manipulation, poor service, and consumer exploitation. When a public utility, or the like, receives a license for monopoly status, it is coupled with regulation in the form of government oversight. One example is the case with the citizens’ utility board that must monitor service and oversee price increases. Call your local cable company in search of service and tell me how this is working in real life…not!

I've spent my career in industrial distribution/fabrication/engineering, and early on, through the trade association, attempted to model industry economic performances for benchmarking proposes. The challenge I encountered was that ours was an industry that had both public and private representation. Simply stated, public companies seek to maximize earnings to enhance the ability to generate a return to the shareholders. Private companies, while not all but in many cases, are seeking to break even. It is sometime called a “profitless prosperity.” After all, why would an owner prefer a double taxed dividend over a performance bonus that is tax deductible?

Returning to the monopoly for the moment, as dangerous as it is, there is indeed something far more dangerous, and that would be the State Owned Enterprise (SOE). I challenge you to share with me any SOE that runs more efficiently than the private sector, which must live or die by the free market forces. While even charities have no obligation to generate profit, they do have mathematic goals, even if such is to simply break even. However, SOEs are under no such pressure. They exist for the pride of the government or nation; they exist to create employment for the masses. To facilitate the aforementioned, they are subsidized by their government. The result is they not only export their steel, but they are also exporting their unemployment, which leads to the disruption of the otherwise efficient forces of a free and fair market.

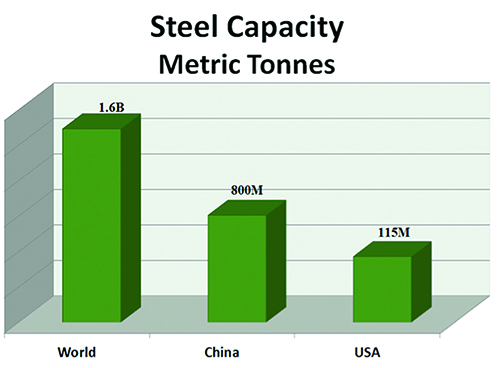

I am not a protectionist who subscribes to the “my country right or wrong axiom.” I am a free market proponent. Should we as a nation, industry or company get beat on a level playing field then shame on us. However, is it even possible to compete when the deck is significantly stacked against us? Therefore, let me bump the needle to the issue at hand. The world’s steel capacity, as reflected in the following graph, has world capacity at 1.6 billion metric tonnes, China has a remarkable 800 million tonnes of such, while we in the U.S. a mere 115 million tonnes.

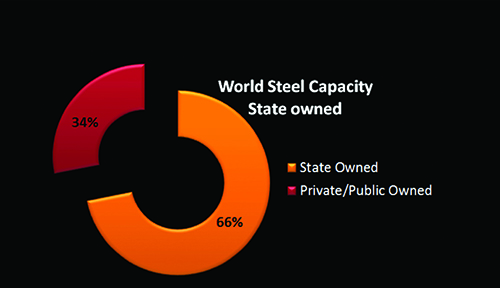

What if we invested our time, effort, energy, money, or in effect our very lives’ to run a widget business, then one day someone entered our livelihood without the obligation to earn a profit? In fact, all deficits would be underwritten. In this all too real example, that competitor would be totally removed from the obligation to generate profit or even run his enterprise efficiently. How would anyone in the world compete with that scenario? That is precisely the problem! As the following graph will reflect, we have now reached the point where 66% of the world’s steel capacity is state owned, and that my friend is the true “root” cause of our problem.

Is there any wonder our industry continues to experience this protracted recession of limited profit or even the absence of such with no end in sight.

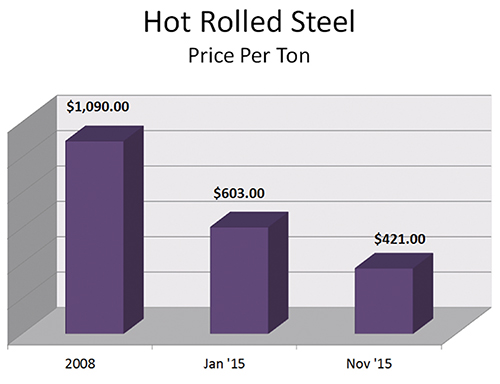

Historically, a manufacturing environment needed to operate at 80% capacity utilization to breakeven. Currently we are at 70% capitalization on a world basis. Traditionally, $600 per ton was breakeven for a manufacturer. Granted, between the cascading prices of commodities and our industry’s impressive efficiencies, this number has fallen significantly. However, $420 per ton (as of this writing) is not an economically sustainable level. Also, when does the organization receive a return on the investments it makes to secure those impressive efficiencies? After all, does one ever invest to lose less! Let me put the problem in the clearest perspective possible: 2 of 3 tons of steel-making capacity in the world has no obligation to be filled properly.

Let me ask the light bulb question…do you really believe China can produce and sell steel today at $260 per ton and cover their costs? But then again, one is under no such obligation when one is state owned. Therefore, to you, my hardworking colleagues of this great industry, let us go forward individually, and in aggregate to deliver this education to our legislators. They must understand the enemy. That enemy must be neutralized by the legitimate enforcement of our trade laws – trade laws already on the books. Level the field and watch us dominate. Failure to act will have negative results for generations to come. Should the later be the case, then shame on us for it will have happened on our watch.

“Vote for the man who promises the least; he’ll be the least disappointing.”

— Bernard Baruch

For more exclusive content, read this article in the November digitial edition.

Featured Video

WHY CHOOSE A JJM® CONDENSATE NEUTRALIZER

Industry Events

-

29Apr

BLUE HAWK 2024 Annual Conference

Denver, CO -

06May

2024 AD Decorative Brands Annual Meeting

Dallas, TX -

14May

2024 EWTS

Scottsdale, AZ